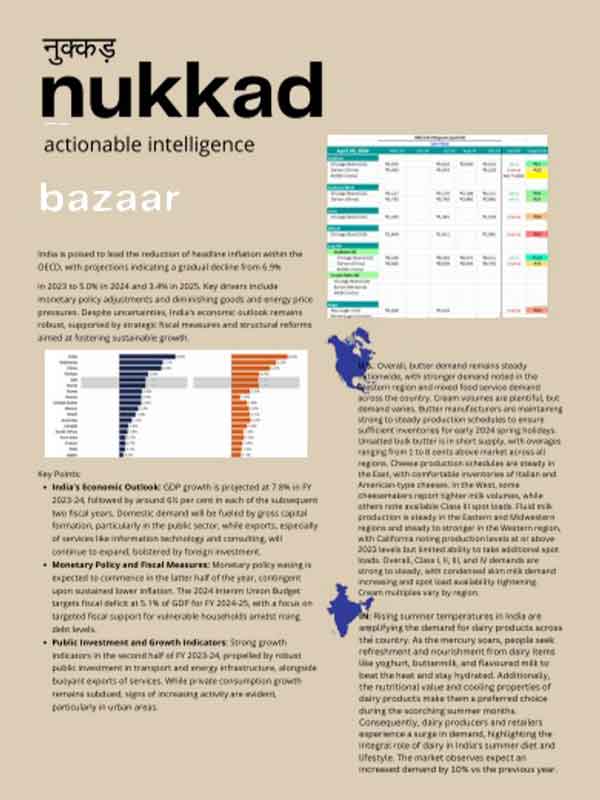

The March 18, 2025, GDT auction continues to reflect a dynamic dairy market, with the GDT Price Index showing mixed performance across products. Over the past 12 months (with a 3-month lag), the weighted average price changes highlight both growth and declines, driven by shifting demand and supply constraints.

Key Highlights

- Whole Milk Powder (WMP): +0.2% to $4,052/MT; year-over-year surge of 36% to a seven-year high of $4,364/MT (as noted previously).

- Skim Milk Powder (SMP): -0.4% to $2,729/MT, a slight decline despite earlier gains of +1.8% to $2,900/MT.

- Butter: +1.1% to $7,667/MT; up 43% year-over-year, reinforcing strong global demand for dairy fats.

- Anhydrous Milk Fat (AMF): -1.8% to $6,561/MT, a more significant drop compared to the earlier -0.5% to $5,600/MT.

- Cheddar: +1.0% to $4,976/MT, slightly below the earlier +1.2% to $4,100/MT.

- Mozzarella: +5.1% to $4,704/MT, a standout performer indicating rising demand for cheese products.

- Lactose: +0.5% to $1,165/MT, showing modest growth.

- Butter Milk Powder (BMP): Data not available (n.a.).

The mixed results—gains in butter, mozzarella, and cheddar contrasted by declines in AMF and SMP—suggest a market balancing strong demand for dairy fats and cheeses against softening powder prices, likely due to supply adjustments or regional demand shifts.

Regional Buying Trends: Market Insights from the World Map

Analysis of NZX and GDT data reveals distinct regional buying patterns, which remain consistent despite the updated auction results:

- North Asia (32%): Dominated by China, this region drives demand for WMP and infant formula, though the slight WMP price increase (+0.2%) and SMP decline (-0.4%) may reflect a stabilization in demand.

- Europe (22%): A stable market with consistent imports, favoring specialty products like mozzarella (+5.1%) and organic dairy.

- Southeast Asia/Oceania (20%): Growing purchases of cheese (e.g., mozzarella, cheddar) align with fast-food expansion, despite softer SMP prices.

- Middle East (14%): Strong demand for long-shelf-life products like UHT milk and powdered milk, though AMF’s decline (-1.8%) may impact costs.

- South America (6%) & Africa (5%): Moderate buying constrained by economic and logistical challenges.

- North America (1%): Minimal participation due to domestic self-sufficiency.

Temporal Trends

A stacked area chart from GDT and Westpac data highlights:

- North Asia: Consistently leads (30%-50%), with peaks in mid-2022 and early 2024 tied to holiday stockpiling (e.g., Chinese New Year). The modest WMP price rise suggests steady but not aggressive buying.

- Southeast Asia & Middle East: Volatile, with spikes in late 2022 and mid-2024. The strong mozzarella price increase (+5.1%) may reflect growing cheese demand in these regions.

- Europe: Stable at 5%-15%, with mozzarella and butter gains indicating a preference for value-added products.

These trends suggest Fonterra should continue prioritizing North Asia’s steady demand, capitalize on cheese demand in Southeast Asia and the Middle East, and leverage Europe’s stable interest in premium dairy.

Factors Driving Price Movements

1. Strong Demand from Asia

- China’s Role: North Asia’s 32% market share is driven by China, where demand for WMP remains steady (+0.2%), though SMP’s decline (-0.4%) may signal a shift toward domestic production or alternative proteins. An aging population and government campaigns promoting dairy for the elderly sustain demand for fortified products.

- Southeast Asia: The significant rise in mozzarella (+5.1%) and cheddar (+1.0%) prices reflects growing fast-food penetration and Western dietary influences.

- Europe: Steady imports, with a notable uptick in butter (+1.1%) and mozzarella, indicate a preference for premium and sustainable dairy products.

2. Supply Constraints

- Weather Challenges: Droughts reduced New Zealand’s 2024 milk production by 2.5%, particularly in Waikato, while Europe’s summer heatwaves cut yields by up to 5% in France and Germany. These constraints likely contribute to the declines in AMF (-1.8%) and SMP (-0.4%), as production prioritizes high-value products like butter and cheese.

- Rising Costs: Energy price hikes, worsened by Eastern European conflicts, have increased processing and transport costs. Feed and fertilizer prices continue to pressure farm margins, impacting powder production.

- Labor Shortages: Post-pandemic migration limits have caused a 10-15% workforce gap in New Zealand and Australia, hindering production capacity.

3. Currency & Geopolitical Stability

- Weaker US Dollar: A 10% depreciation historically lifts dairy prices by 5-7%, enhancing affordability for non-US buyers. This trend supports gains in butter, mozzarella, and cheddar.

- Geopolitical Risks: Stability has aided trade predictability, but risks loom—South China Sea tensions could disrupt shipping, while US-China trade disputes or the Ukraine conflict may raise costs via tariffs or energy price volatility.

Implications for Fonterra and the Dairy Market

1. Benefits for Fonterra & Farmers

- Higher Farmgate Milk Prices: Despite mixed results, the earlier forecast of NZ$7.90/kgMS remains plausible, driven by strong butter (+1.1%) and mozzarella (+5.1%) prices, boosting farmer incomes.

- Financial Strength: Gains in high-value products like butter and cheese enhance Fonterra’s margins, providing capital for innovation.

- GDT Pulse Expansion: More frequent auctions improve market liquidity and responsiveness, particularly for volatile products like mozzarella.

2. Risks & Challenges

- Economic Uncertainties: A potential slowdown in China or recessions in key markets could dampen demand, especially for powders (SMP -0.4%).

- Supply Chain Vulnerabilities: Shipping delays, regulatory shifts, or climate disruptions remain threats, particularly for AMF (-1.8%).

Insights from CLAL & Market Analysis

- Tightening Supply: Production declines in New Zealand and Europe align with GDT trends, particularly impacting AMF and SMP availability.

- Rising Input Costs: Persistent increases in energy, fertilizer, and feed costs challenge profitability, especially for powder production.

- Sustainability Trends: Consumers and regulators (e.g., EU Green Deal, China’s carbon goals) demand eco-friendly practices. Fonterra’s 30% emissions cut since 2015 and net-zero 2050 target position it well, but competitors like Danone (100% regenerative farms by 2030) are advancing.

Conclusion & Strategic Takeaways

The March 2025 GDT auction reflects a complex dairy market, with strong demand for dairy fats (butter +1.1%) and cheeses (mozzarella +5.1%, cheddar +1.0%) offset by declines in powders (SMP -0.4%, AMF -1.8%). Fonterra’s GDT Pulse initiative demonstrates agility, but risks like geopolitical instability and supply chain fragility require proactive management. Below are refined, actionable strategies: